Market Recap for Wednesday, February 6, 2019

All of our major indices closed lower on Wednesday and we haven't seen that very often in 2019. The losses were minimal and traders continued to have an appetite for the riskier sectors, so it certainly wasn't a huge win for the bears. But down is down and a downtrend cannot begin without a start. I wouldn't worry too much from a bullish perspective so long as price action remains above the rising 20 day EMA. If we move below, then I'd at least become more cautious:

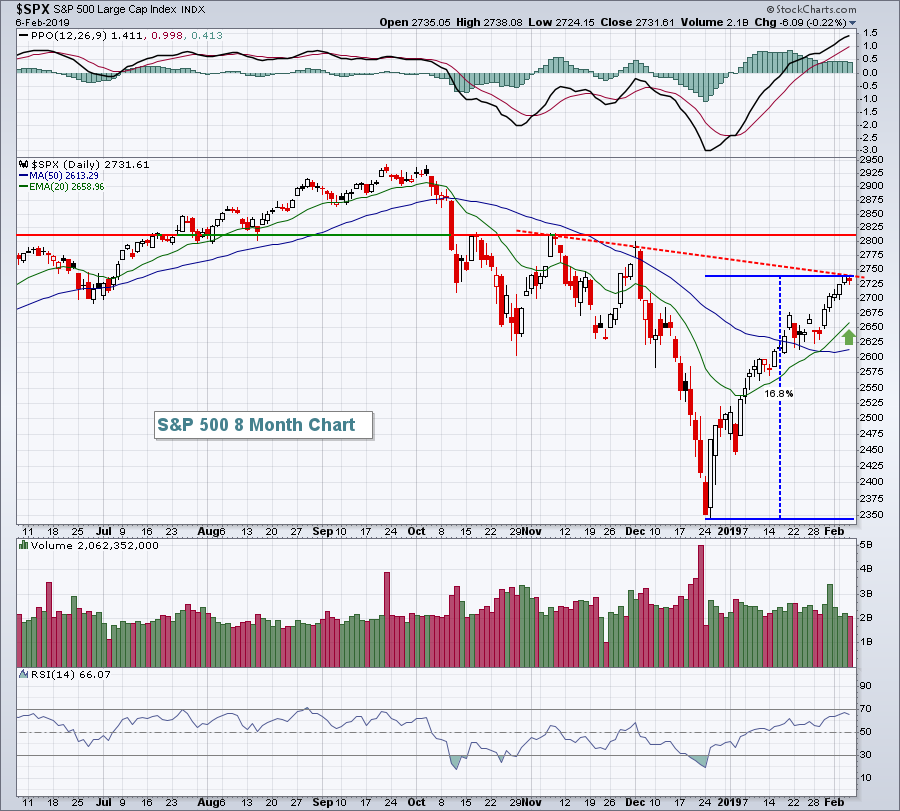

The rally off the December 26th low is nearly 17%. A move up of 20% or more would constitute a new bull market. A bear market in December followed by a bull market the following February doesn't seem like reality, but cyclical bear markets do not last long - certainly not nearly as long as secular bear markets. Still, history has shown us that the past two cyclical bear markets in 1998 and 1990 both saw retests of initial lows minimally. I'm beginning to doubt we'll see that because a few factors, most notably the drop in the Volatility Index ($VIX) beneath 16. The VIX closed at 15.38. While Wall Street can rewrite the record books at any time, it should be noted that the VIX doesn't typically fall beneath 16 during bear markets. It did not during either of the last two secular bear markets, nor the prior two cyclical bear markets. So a move to a new S&P 500 cyclical bear market low after the VIX has fallen beneath 16 would represent something different for sure.

The rally off the December 26th low is nearly 17%. A move up of 20% or more would constitute a new bull market. A bear market in December followed by a bull market the following February doesn't seem like reality, but cyclical bear markets do not last long - certainly not nearly as long as secular bear markets. Still, history has shown us that the past two cyclical bear markets in 1998 and 1990 both saw retests of initial lows minimally. I'm beginning to doubt we'll see that because a few factors, most notably the drop in the Volatility Index ($VIX) beneath 16. The VIX closed at 15.38. While Wall Street can rewrite the record books at any time, it should be noted that the VIX doesn't typically fall beneath 16 during bear markets. It did not during either of the last two secular bear markets, nor the prior two cyclical bear markets. So a move to a new S&P 500 cyclical bear market low after the VIX has fallen beneath 16 would represent something different for sure.

Yesterday, healthcare (XLV, +0.45%) and technology (XLK, +0.34%) were the clear market leaders. Communication services (XLC, -2.24%) took a 1-2 punch from media agencies ($DJUSAV, -4.74%) and internet ($DJUSNS, -1.62%) to lag the broader market. Interpublic Group of Cos. (IPG, -5.63%) and Omnicom Group (OMC, -4.98%) were the media agency culprits. In the DJUSNS, Electronic Arts (EA, -13.31%), Take-Two Interactive Software (TTWO, -13.76%) and Activision Blizzard (ATVI, -10.12%) were hurt by the combination of disappointing quarterly results and weak outlooks.

Pre-Market Action

The 10 year treasury yield ($TNX) remains problematic as it dips another 3 basis points this morning to 2.67%. Money rotating into defensive treasuries lowers yields and signals a "risk off" environment, which typically is not good for equities. Crude oil ($WTIC) is down more than 1%, while gold ($GOLD) is flat.

In global market action, Asian markets were mixed overnight, but European markets are being hit rather hard, especially in Germany where the German DAX ($DAX) is currently lower by 206 points, or 1.82%. Weakness in Germany can be a problem for U.S. stocks as the two countries' equity market have a history of strong positive correlation.

Dow Jones futures, not too surprisingly, are lower by 135 points with 30 minutes left to the opening bell.

Current Outlook

I know the relative strength of consumer discretionary stocks (XLY) struggled vs. its more defensive consumer staples counterpart (XLP), but it was really a return to normalcy more than anything else. The XLY:XLP accelerated in unsustainable fashion throughout the first half of 2018, so the XLY has paid the piper since then:

Through my experience, the XLY:XLP ratio has been one of the best intermarket relationships to watch in determining the sustainability (or lack thereof) of an S&P 500 directional move. I believe the current XLY:XLP uptrend is one to keep a close eye on in 2019 and beyond. We want to see traders in a "risk on" mode to sustain rallies and a rising XLY:XLP is a very solid signal of "risk on".

Through my experience, the XLY:XLP ratio has been one of the best intermarket relationships to watch in determining the sustainability (or lack thereof) of an S&P 500 directional move. I believe the current XLY:XLP uptrend is one to keep a close eye on in 2019 and beyond. We want to see traders in a "risk on" mode to sustain rallies and a rising XLY:XLP is a very solid signal of "risk on".

Sector/Industry Watch

Restaurants & bars ($DJUSRU) have been quite strong since the 2009 bull market began, but the relative strength over the past several months has really picked up:

The blue circles highlight periods during relative uptrends where we see temporary periods of relative underperformance. I believe we're in one of those right now, but are likely to break to the upside again soon. Also, the current bullish up channel remains perfectly intact and illustrates the strength of an uptrend with multiple successful tests along the way (blue arrows). Continue to consider trading/owning best of breed restaurant & bar stocks. A great place to start would be the highest ranking SCTRs among this industry group.

The blue circles highlight periods during relative uptrends where we see temporary periods of relative underperformance. I believe we're in one of those right now, but are likely to break to the upside again soon. Also, the current bullish up channel remains perfectly intact and illustrates the strength of an uptrend with multiple successful tests along the way (blue arrows). Continue to consider trading/owning best of breed restaurant & bar stocks. A great place to start would be the highest ranking SCTRs among this industry group.

Historical Tendencies

Since 1971, February (+7.81%) ranks as the 7th best calendar month in terms of NASDAQ annualized performance. But this decade, February has been exceptionally strong, producing annualized returns of +34.69%, second only to July's +36.00%.

Key Earnings Reports

(actual vs. estimate):

BCE: .67 vs .66

CAH: 1.29 vs 1.09

FCAU: 1.02 - estimate, awaiting results

FUJIY: .75 vs .96

ICE: .94 vs .92

LH: 2.52 vs 2.48

K: .91 vs .88

MPC: 2.41 vs 1.98

MPLX: .52 vs .68

PM: 1.16 - estimate, awaiting results

SNY: .63 vs .62

SPGI: 2.22 vs 2.20

TMUS: .75 vs .69

TSN: 1.58 vs 1.55

TWTR: .31 vs .25

WLTW: 4.00 vs 4.06

YUM: .40 vs .97

(reports after close, estimate provided):

DXC: 2.04

EXPE: 1.07

FISV: .84

FTV: .86

IAC: .99

MSI: 2.49

MTD: 6.74

RSG: .78

VRSN: 1.21

Key Economic Reports

Initial jobless claims released at 8:30am EST: 234,000 (actual) vs. 223,000 (estimate)

Happy trading!

Tom