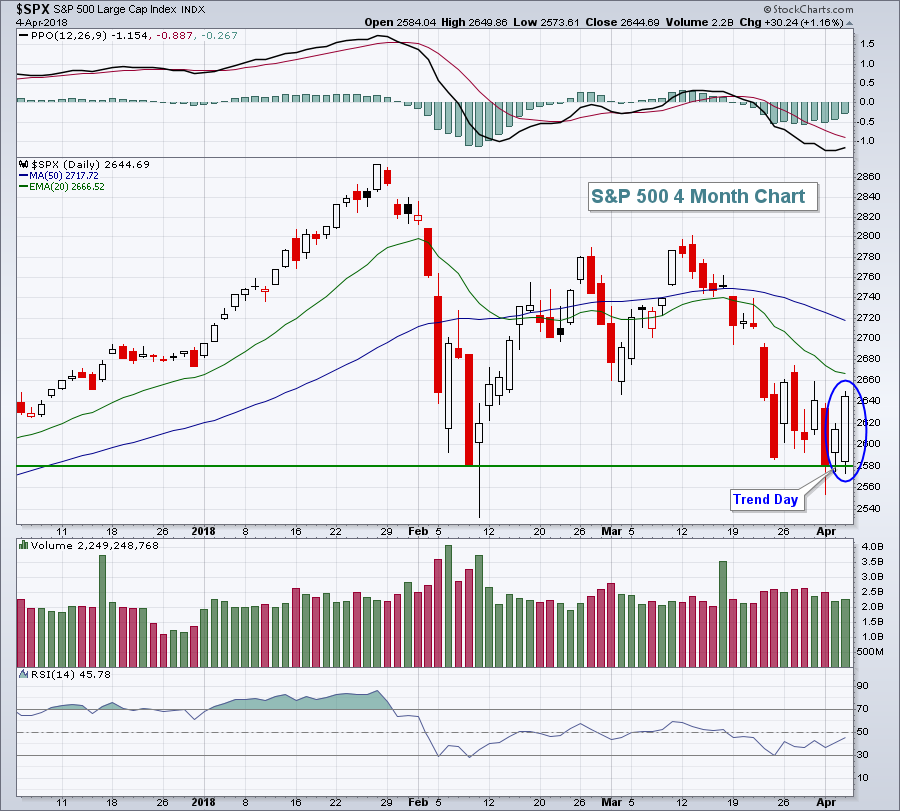

Market Recap for Wednesday, April 4, 2018

Welcome back consumer stocks! One day certainly doesn't make a fresh new trend, but it's been awhile since consumer stocks led a rally. Consumer discretionary (XLY, +1.84%) and consumer staples (XLP, +1.56%) were atop the sector leaderboard on Wednesday as our major indices rallied throughout the session after another trade war-related scare at the open. China announced new tariffs against U.S. products and futures tumbled several hundred points as a result. We threatened yet another short-term breakdown, but this time support held and buyers re-emerged to orchestrate a "trend" day, where buying is met with more buying throughout the day. Trend days are characterized by long hollow candles showing that price action opened on or near its low and finished on or near its high:

There's more on the consumer discretionary sector in the Sector/Industry Watch section below.

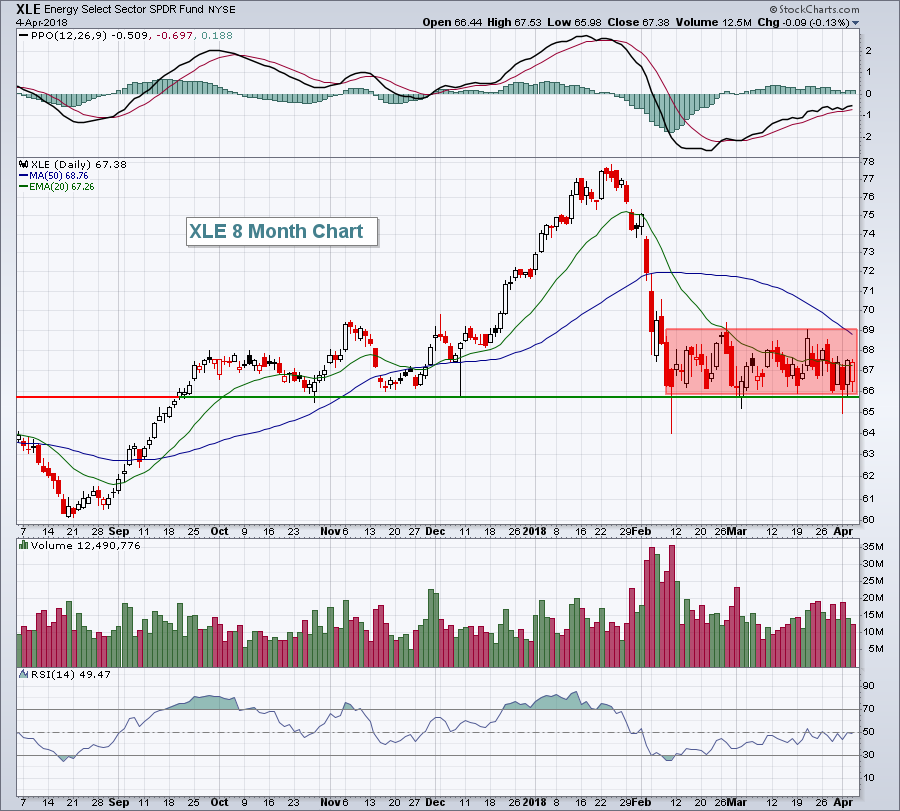

Eight of nine sectors advanced yesterday with only the disappointing energy space (XLE, -0.13%) lagging. Crude oil prices ($WTIC), which as recently as one week ago were testing key overhead resistance at $66 per barrel, have fallen in recent sessions, nearly touching $62 per barrel on Wednesday. The sudden decline in the WTIC is certainly not helping the XLE's bid to break out and rid itself of the two months of painful consolidation between 66.00-69.00:

A close back above 69.00 that holds rising 20 day EMA support is what the energy bulls are hoping for.

A close back above 69.00 that holds rising 20 day EMA support is what the energy bulls are hoping for.

Pre-Market Action

Despite a higher-than-expected initial jobless claims number (242,000 vs 230,000), futures are pointing to a continuation of Wednesday's bullish action. Trade war fears seem to have settled down as Dow Jones futures suggest a triple digit gain at the opening bell in nearly an hour.

The 10 year treasury yield ($TNX) has climbed back above 2.80%, currently at 2.81%, and that should help financials (XLY) hold onto key price support at 26.70. That's the support level to watch and short-term resistance is at the declining 20 day EMA, currently at 27.95.

Asian markets were solid overnight with the Tokyo Nikkei ($NIKK) up 325 points, or 1.53%. Both China's Shanghai Composite ($SSEC) and Hong Kong's Hang Seng Index ($HSI) were closed for the Ching Ming Festival.

In a very bullish development, European markets are significantly higher this morning with German DAX ($DAX) up 2.34% at last check. That is above its 20 day EMA and a close there today would be only the third such close since the big selling began more than two months ago.

Of course, the biggest obstacle for the bulls is the Volatility Index ($VIX). Fear breeds selling and the VIX did still close yesterday at 20.06. For the bulls to truly gain control of the action, we need to see the VIX move to a level that clears early March support just beneath 15.

Current Outlook

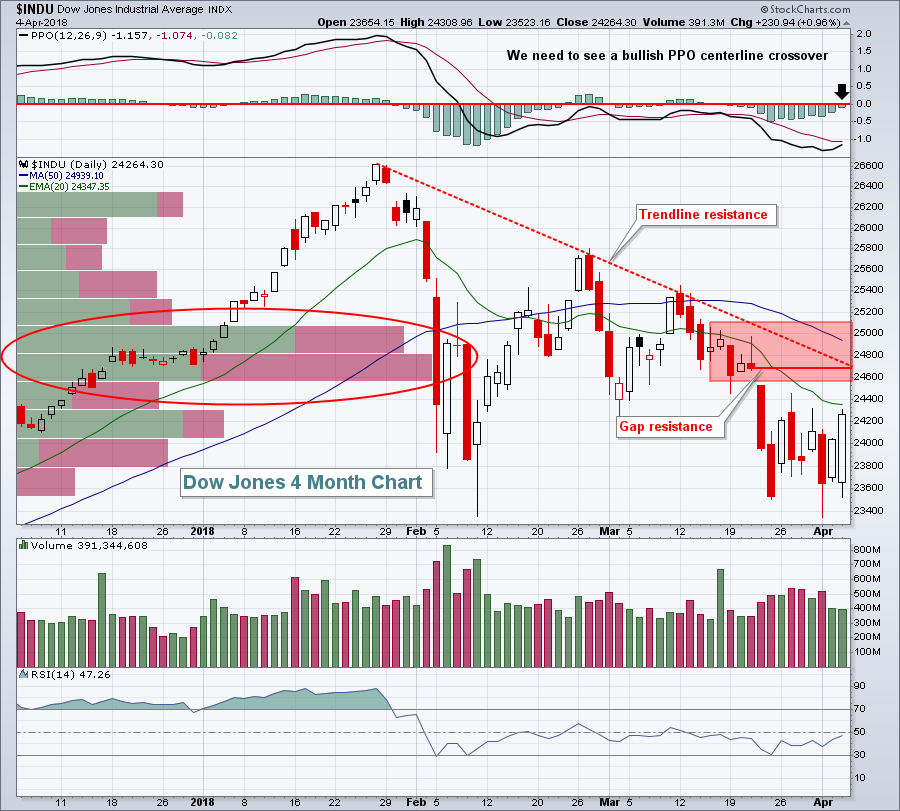

While Wednesday's action felt great, the "volume by price" indicator shows that the Dow Jones has serious overhead price resistance to negotiate before the cloudy skies begin to clear:

I've been bullish throughout this consolidation period, mostly because my "below the surface" signals have not turned bearish at all. But being bullish doesn't translate into "the stock market is going higher right now". We're dealing with the overbought conditions that were left from the last high in January. We've got momentum issues in the near-term as evidenced by the PPO remaining below its centerline for the past two months, we have been failing at the declining 20 day EMA for the past few weeks and the volume by price indicator shows significant overhead price resistance (red shaded area) from approximately 24600-25100. Throw in gap resistance and trendline resistance, both of which are currently intersecting near 24700 and you can see that this is not likely to be an easy battle for the bulls, although I do believe the battle will ultimately be won by the bulls.

I've been bullish throughout this consolidation period, mostly because my "below the surface" signals have not turned bearish at all. But being bullish doesn't translate into "the stock market is going higher right now". We're dealing with the overbought conditions that were left from the last high in January. We've got momentum issues in the near-term as evidenced by the PPO remaining below its centerline for the past two months, we have been failing at the declining 20 day EMA for the past few weeks and the volume by price indicator shows significant overhead price resistance (red shaded area) from approximately 24600-25100. Throw in gap resistance and trendline resistance, both of which are currently intersecting near 24700 and you can see that this is not likely to be an easy battle for the bulls, although I do believe the battle will ultimately be won by the bulls.

Sector/Industry Watch

Consumer stocks were very strong on Wednesday and futures are pointing higher this morning. The consumer discretionary group (XLY) was a clear relative leader during the last rally that led to the January top. A positive signal would be the XLY's ability to close back above its 20 day EMA:

Despite a weakening market over the past two months, the XLY's relative strength has printed higher lows with an equal high - a relative ascending triangle. That would not be expected at the start of a bear market. We would likely see relative weakness from aggressive areas like consumer discretionary. This chart supports the notion that we are in a correction with our next major market move higher.

Despite a weakening market over the past two months, the XLY's relative strength has printed higher lows with an equal high - a relative ascending triangle. That would not be expected at the start of a bear market. We would likely see relative weakness from aggressive areas like consumer discretionary. This chart supports the notion that we are in a correction with our next major market move higher.

Historical Tendencies

Advanced Micro Devices (AMD) has historically shown much strength during March, April and May as it's posted average monthly returns of +5.3%, +3.9% and 4.6%, respectively, over the past two decades. I mention this because AMD broke to a 15 month low at yesterday's open before printing a reversing bullish engulfing candlestick:

Initial resistance on any rally would likely be felt at the declining 20 day EMA (red arrow).

Initial resistance on any rally would likely be felt at the declining 20 day EMA (red arrow).

Key Earnings Reports

(actual vs. estimate):

MON: 3.22 vs 3.38

Key Economic Reports

Initial jobless claims released at 8:30am EST: 242,000 (actual) vs. 230,000 (estimate)

Happy trading!

Tom