Market Recap for Thursday, November 11, 2016

First let me say a heartfelt thank you to all our veterans today for your service - past, present and future. Please thank those that protected or protect our freedoms every day.

Financials (XLF, +3.69%) and industrials (XLI, +2.13%) once again led in a big, big way on Thursday as traders contemplate how a Trump presidency will affect the U.S. stock market. President-elect Trump has suggested he'll be committed to infrastructure. Heavy construction ($DJUSHV) had been languishing in a sideways consolidation pattern prior to the election, but check out the reaction in the group the past two sessions:

Consumer stocks were weak yesterday. While consumer discretionary (XLY, +0.37%) held up okay, its staples counterpart (XLP, -2.67%) had a very rough day. So money wasn't rotating towards consumer stocks overall, but the XLY:XLP ratio strengthened, which is bullish on a market advance. Higher treasury yields negatively impact dividend paying stocks so both consumer staples and utilities (XLU, -2.41%) struggled mightily recently with the 10 year treasury yield ($TNX) surging.

Consumer stocks were weak yesterday. While consumer discretionary (XLY, +0.37%) held up okay, its staples counterpart (XLP, -2.67%) had a very rough day. So money wasn't rotating towards consumer stocks overall, but the XLY:XLP ratio strengthened, which is bullish on a market advance. Higher treasury yields negatively impact dividend paying stocks so both consumer staples and utilities (XLU, -2.41%) struggled mightily recently with the 10 year treasury yield ($TNX) surging.

If the S&P 500 rise continues and we see a breakout, I want to see certain relative ratios rising with it. Take a look at this chart:

This behavior is clearly bullish in my view. Not only is the uptrend in play on the S&P 500, but money has been rotating towards aggressive areas of the market, especially over the past couple trading sessions. In other words, market participants are not gearing up for a market meltdown so neither should we. Obviously keep stops in place, but as far as which side of the trade I want to be on, it's definitely on the long side right now with recent technical developments.

This behavior is clearly bullish in my view. Not only is the uptrend in play on the S&P 500, but money has been rotating towards aggressive areas of the market, especially over the past couple trading sessions. In other words, market participants are not gearing up for a market meltdown so neither should we. Obviously keep stops in place, but as far as which side of the trade I want to be on, it's definitely on the long side right now with recent technical developments.

Pre-Market Action

U.S. futures are pointing to profit taking at the opening bell as Dow Jones futures are lower by 29 points with a bit more than 30 minutes of pre-market action left. In Asia overnight, the Hang Seng ($HSI) lost over 300 points, but is in a bullish wedge in my view. I'd look for 22200 to hold as price support. In Europe, the German DAX ($DAX) touched 10800 resistance yesterday before it was met with selling. The DAX is fractionally higher this morning, helping to offset weakness in London where the FTSE has fallen 1.2% this morning. I'd expect to see the FTSE hold 6600 support.

Current Outlook

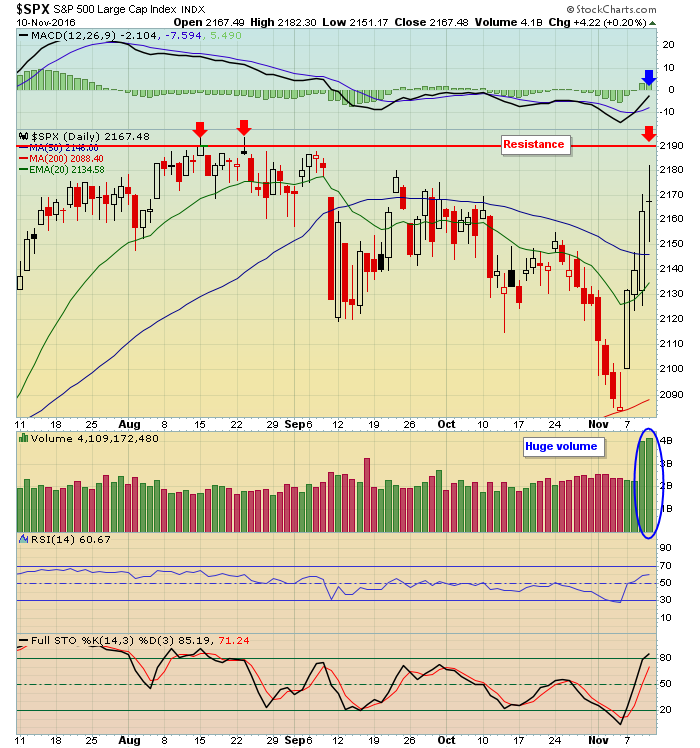

I'm sure there's one nagging stock market question all of us are asking ourselves right now. Should we trust this rally? Honestly, it's not an easy question to answer. There are compelling arguments on both sides. It seems almost unfathomable that the benchmark S&P 500 resides just one percent from an all-time high after all the news of late, but is that telling us something? Let me re-emphasize one very important technical factor. Nothing in my view is more important than the combination of price and volume. Over the past two trading sessions, that combination has been firmly in the bulls' camp. Take a look at the surge of volume to accompany recent price action:

The rally has been great, there's not much doubt about that. The blue circle shows very heavy volume so it's difficult to argue that the rally isn't being supported by institutions. Daily MACD does remain in negative territory so I'd like to see two things to feel better about this rally. First, I want to see the strong volume continue and the S&P 500 close above 2190. Second, and this should occur if the bullish close occurs, I want to see a bullish MACD crossover suggesting that price momentum has turned bullish. The only thing left after that is to evaluate the underlying strength of the move in terms of sector rotation and participation. I've laid out what to look for in that regard above in the Market Recap section.

The rally has been great, there's not much doubt about that. The blue circle shows very heavy volume so it's difficult to argue that the rally isn't being supported by institutions. Daily MACD does remain in negative territory so I'd like to see two things to feel better about this rally. First, I want to see the strong volume continue and the S&P 500 close above 2190. Second, and this should occur if the bullish close occurs, I want to see a bullish MACD crossover suggesting that price momentum has turned bullish. The only thing left after that is to evaluate the underlying strength of the move in terms of sector rotation and participation. I've laid out what to look for in that regard above in the Market Recap section.

Sector/Industry Watch

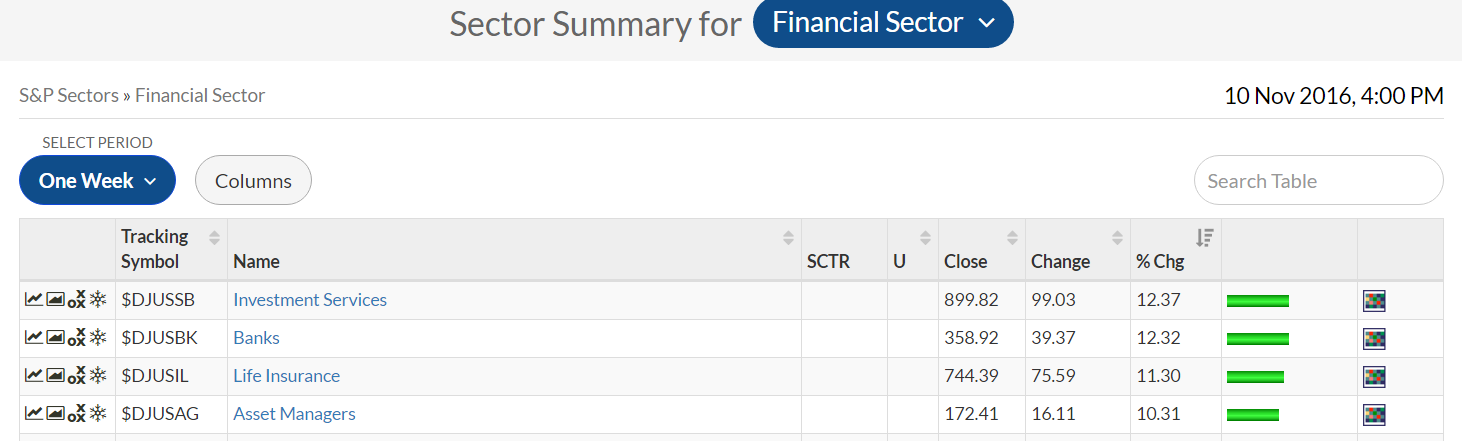

I've discussed the strong relative performance of financials quite a bit lately, but I've primarily focused on banks ($DJUSBK) and life insurance ($DJUSIL) companies. The best performer in financials during this recent rally, however, has been investment services ($DJUSSB). Take a look at the financials leaderboard over the past week:

These are the groups that you want to see lead in the financial space, especially banks. If the economy were weakening or market participants were anticipating the weakening of our economy, we'd see a rush to treasuries (as opposed to equities) with treasury yields falling and credit worthiness of companies would be declining, resulting in higher loan loss reserves for banks. That combination leads to much lower bank profits and relative underperformance by the industry. That simply isn't what the market is telling us right now. Instead, banks have been thriving and leading on a relative basis. The 10 year treasury yield ($TNX) has been soaring and that leads to widening net interest margins, potentially lower loan loss reserves and higher EPS for banks. That's why traders are rushing into the group right now. Despite all of this, however, investment services are leading the financial rush. Check out the technical outlook:

These are the groups that you want to see lead in the financial space, especially banks. If the economy were weakening or market participants were anticipating the weakening of our economy, we'd see a rush to treasuries (as opposed to equities) with treasury yields falling and credit worthiness of companies would be declining, resulting in higher loan loss reserves for banks. That combination leads to much lower bank profits and relative underperformance by the industry. That simply isn't what the market is telling us right now. Instead, banks have been thriving and leading on a relative basis. The 10 year treasury yield ($TNX) has been soaring and that leads to widening net interest margins, potentially lower loan loss reserves and higher EPS for banks. That's why traders are rushing into the group right now. Despite all of this, however, investment services are leading the financial rush. Check out the technical outlook:

Surprisingly, the DJUSSB broke out just prior to the election. The reaction since, though, is quite evident and powerful. Institutions are accumulating investment services companies and that volume is sending a very strong message. The biggest problem currently is that many industries within financials have moved up so much that they're now extremely overbought. In the short-term, it would be prudent to see profit taking in the group before considering entry or additional commitment.

Surprisingly, the DJUSSB broke out just prior to the election. The reaction since, though, is quite evident and powerful. Institutions are accumulating investment services companies and that volume is sending a very strong message. The biggest problem currently is that many industries within financials have moved up so much that they're now extremely overbought. In the short-term, it would be prudent to see profit taking in the group before considering entry or additional commitment.

Historical Tendencies

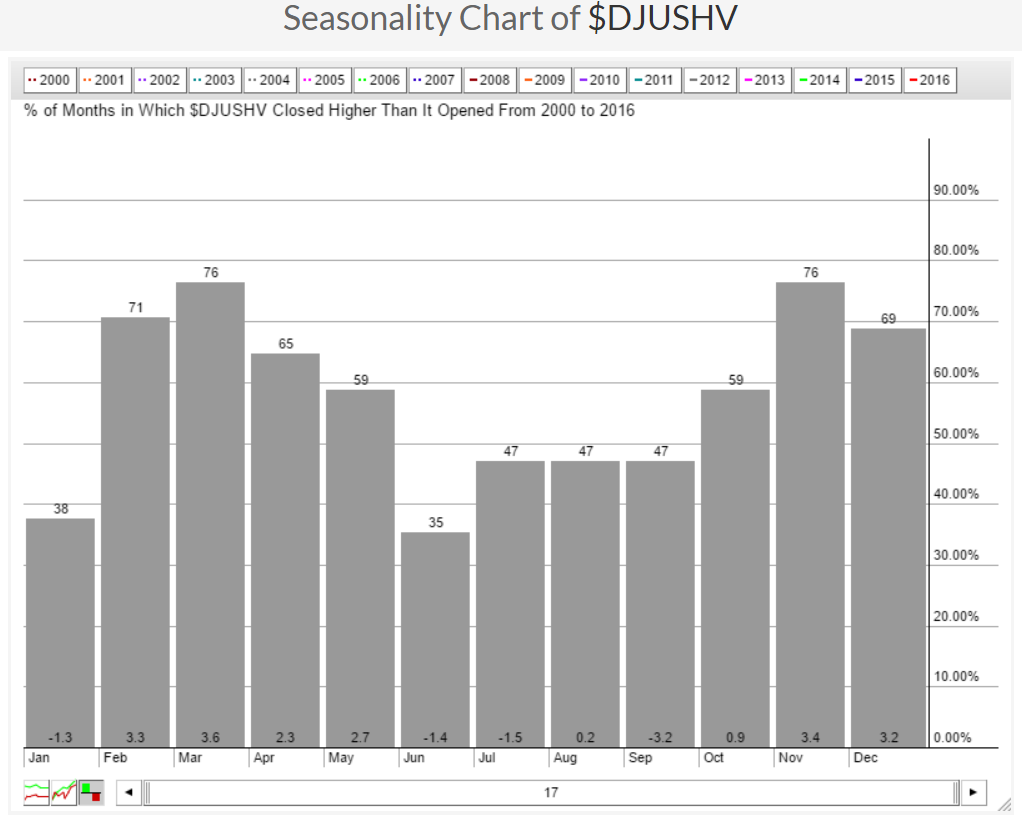

I wrote earlier about the heavy construction industry with its price breakout. Strength this time of year for the group also makes sense. Here's the seasonal behavior by calendar month for the DJUSHV over the past 17 years:

Beginning in November, the DJUSHV has averaged at least a 2.3% gain in every month through May (except January). That's strong historical tailwinds to support the current technical breakout. Consider this industry group carefully given this backdrop.

Beginning in November, the DJUSHV has averaged at least a 2.3% gain in every month through May (except January). That's strong historical tailwinds to support the current technical breakout. Consider this industry group carefully given this backdrop.

Key Earnings Reports

(actual vs. estimate):

NTT: 1.13 (actual - no estimate provided)

Key Economic Reports

U.S. Banks are closed today but the stock market is open

November consumer sentiment to be released at 10:00am EST: 87.1 (estimate)

Happy trading!

Tom