Market Recap for Wednesday, September 16, 2015

The bulls continued to piece back together technical conditions on Wednesday ahead of the Fed announcement later today. All sectors finished higher, although it was the outsized gain in energy (XLE) that clearly "fueled" the rally. Coal ($DJUSCL) gained 6% and oil equipment and services ($DJUSOI) added another 3.96% to lead the charge. Both of these industry groups had been reeling for months, however, so the gains could be nothing more than a bounce higher within the confines of a steady downtrend. Technically, the XLE was able to clear its 20 day EMA and you can see from the chart below that's been a rarity since early May:

Selling in treasuries also continued throughout much of the trading session, resulting in the 10 year treasury yield ($TNX) closing above 2.30% for the first time since mid-July. If the Fed decides later today to raise interest rates for the first time in nine years, expect the TNX to make a run at the double top in June close to 2.50%. Here's the visual on the TNX:

Pre-Market Action

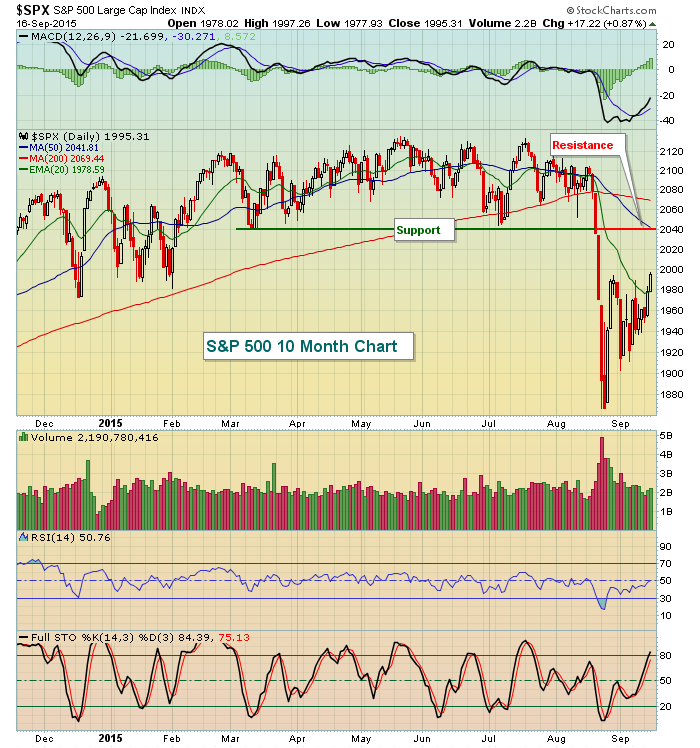

U.S. futures have been mostly lower this morning as anticipation for this afternoon's Fed announcement escalates. On Wednesday, the S&P 500 traded and closed higher than it has at any point since the August high volume breakdown occurred. If traders are disappointed this afternoon, look for a resumption of the earlier downtrend with Wednesday marking the near-term high and critical resistance in the days and weeks ahead. If traders are buoyed by this afternoon's announcement, I'd look for a very quick advance to the 2040 level where both price resistance and the declining 50 day SMA reside.

Not so encouraging has been Germany's (and most of Europe's) inability to track the S&P 500 to fresh new highs from August's selling. Germany, in fact, continues to battle 20 day EMA resistance as shown below and this needs to change:

The DAX needs to clear 10650 to begin to recover from the technical effects of the August selling. As you can see, we've still got a long way to go there and this European headwind will not help the U.S., especially if traders react negatively to the Fed announcement today.

Current Outlook

I'm sticking to my guns. I believe the Federal Reserve should raise rates today. We're only talking about a 25 basis point hike from historically low levels. More than anything else, it would serve as a symbol that the Fed-induced quantitative easing period is finally over. CNBC ran a quck survey among viewers on Wednesday during the trading day and nearly two-thirds agreed with me - that the Fed should raise rates. This afternoon marks perhaps the most widely anticipated Fed meeting over the past couple years and it certainly appears the treasury market is guessing they'll follow through with their prior warnings of a rate hike. Failing to hike rates, or even delaying it, would likely leave traders confused as to where the Fed stands on our slow economic recovery.

While the recent stock market rally may have the appearance of a strong move, I'd be a little apprehensive about jumping to that conclusion. Volume has been light for the most part these past few days with daily volume on the NASDAQ much below 2 billion shares on most occasions. Also, the following intraday chart on the S&P 500 is worthy to note as relative strength in a few key aggressive areas of the market has deteriorated over the past few trading sessions despite an S&P 500 that is "breaking out" above its 20 day EMA and recent price resistance. Check this out:

This picture really tries to tell me a completely different story. Yes, the rally on the S&P 500 the past couple days to clear resistance is noteworthy and bullish, but how do we explain the fact that suddenly over the past few trading sessions money has rotated away from aggressive areas of the market? I look for these ratios to push higher to support a breakout, not fall apart. I'm not suggesting that this chart tells us this rally will fail, but IF IT FAILS, be very very careful as traders appear to be growing a bit more cautious ahead of today's announcement and the VIX remains above 20. The market is NOT prepared to handle disappointment in my view, making 2pm EST that much more interesting. Look for the possibility of EXTREME volatility as prices could swing wildly this afternoon in BOTH directions before price action settles down into a continuing rally or breakdown. Put on your hard hats.

Sector/Industry Watch

Yesterday, I focused on life insurance as that industry group should perform well in a rising interest rate environment. Banks ($DJUSBK) are in that same boat. Rising rates and a steepening yield curve improves net interest margin for banks, a key driver in their profitability. Yet we've seen little bullish action from banks despite the 10 year treasury yield busting through 2.25% resistance. What gives? Well, all is not lost as the long-term picture on banks remains bullish thus far. Have a look:

Banks have not recovered quite as strongly as I would have liked given the rise in treasury yields, but the long-term chart on banks remains quite bullish with a solid uptrend in play. Also, note the weekly momentum has been strong for 3 1/2 years as evidenced by a weekly MACD above centerline support throughout the period. We now show the weekly MACD almost squarely on the zero line, suggesting banks could be poised for a very nice upside move if the Fed cooperates and raises rates later today.

Historical Tendencies

Let's not lose sight of the bearish historical tendencies the U.S. stock market faces this time of year. If the Fed does not provide the market with what it's looking for, the second half of September won't help AT ALL. Beginning next week, here are the daily annualized returns on the NASDAQ since 1971:

September 21 (Monday): -92.11%

September 22 (Tuesday): -83.40%

September 23 (Wednesday): -41.45%

September 24 (Thursday): -18.48%

September 25 (Friday): -53.51%

Key Earnings Reports:

ADBE: $.35 estimate - reports today after the close

RAD: $.04 (actual) vs. $.03 (estimate)

Key Economic Reports:

August housing starts released at 8:30am EST: 1.126 mil units (actual) vs. 1.168 mil units (estimate)

August building permits released at 8:30am EST: 1.170 mil units (actual) vs. 1.160 mil units (estimate)

Initial jobless claims released at 8:30am EST: 264,000 (actual) vs. 275,000 (estimate)

September Philadelphia Fed Survey to be released at 10:00am EST: 6.3 (estimate)

Happy trading!

Tom