Advisors know that setting the right expectations with clients is critical. Investment performance can be an awkward conversation when there isn't clarity between the advisor and client on what the investment benchmark is. When the client knows what they own and why they own it, quarterly meetings are a breeze — and performance is often not even discussed.

2021 was a tough year to explain portfolio return differences because of the sharp outperformance among just a handful of S&P 500 stocks. To be fair, the equal-weight version of the S&P 500 returned about the same as the cap-weighted version, but ex-U.S. stocks and the bond market provided relatively meager returns.

S&P 500: Cap-Weighted and Equal-Weighted Indexes (SPY, RSP) 2021 Performances (29% Total Return)

S&P 500: Cap-Weighted and Equal-Weighted Indexes (SPY, RSP) 2021 Performances (29% Total Return)

SPY, Nasdaq 100 ETF (QQQ) and Ex-U.S. Stocks (VEU) 2021 Performances

SPY, Nasdaq 100 ETF (QQQ) and Ex-U.S. Stocks (VEU) 2021 Performances

That wide dispersion in sub-asset class total return numbers made diversified portfolios appear to be losers versus the S&P 500. When clients flip on financial TV or step into the Fintwit blogosphere, they are inundated with return figures of the Nasdaq and S&P 500. When they read about returns in the 25-30% range for large-cap domestic equities, they might naturally assume that is about what their accounts earned for the year.

Most advisors have likely worked with their clients long enough to where this potential discrepancy is a non-issue, but new advisors scrambling just to manage their business and keep clients satisfied can easily overlook a proper investment benchmarking conversation. Important strategies to keep on the same page include using historical return data, explaining the benefits of diversification, going over the logic of the home bias and underscoring the importance of owning a portfolio that fits the client's risk and return objectives.

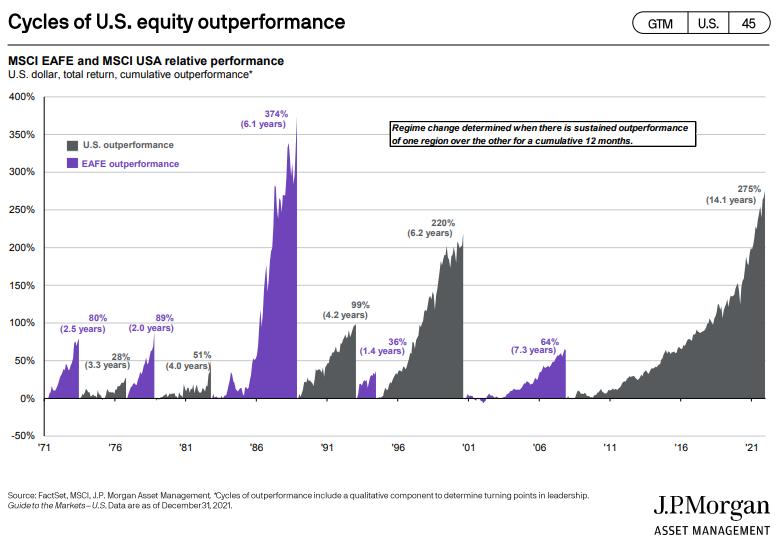

JPM Guide to the Markets: Cycles of U.S. Equity Outperformance

JPM Guide to the Markets: Cycles of U.S. Equity Outperformance

Sure, we all wished we owned a 100% U.S. equity portfolio in 2021 (and over the last 13 years), but when inevitable bear markets happen and as market cycles change, a diversified portfolio will probably provide some cushion for a long-term investor. Moreover, an extremely risky basket of holdings might not be ideal from a behavioral perspective, since a sustained uptick in volatility might cause the retail client to panic and sell at the wrong time.

It is an advisor's duty to help people navigate volatile markets, not by moving in and out of the market but by helping them keep to their long-term strategy. The right time is always "soon" when it comes to getting on the same page about allocation strategy.

Be sure to hop on my CMT Association Educational Webinar on Wednesday, February 9 from 12:00 pm – 1:00 pm ET, where I will discuss how technical analysis can be useful for financial advisors.

Mike Zaccardi, CFA, CMT

Investment Writer, Zaccardi LLC