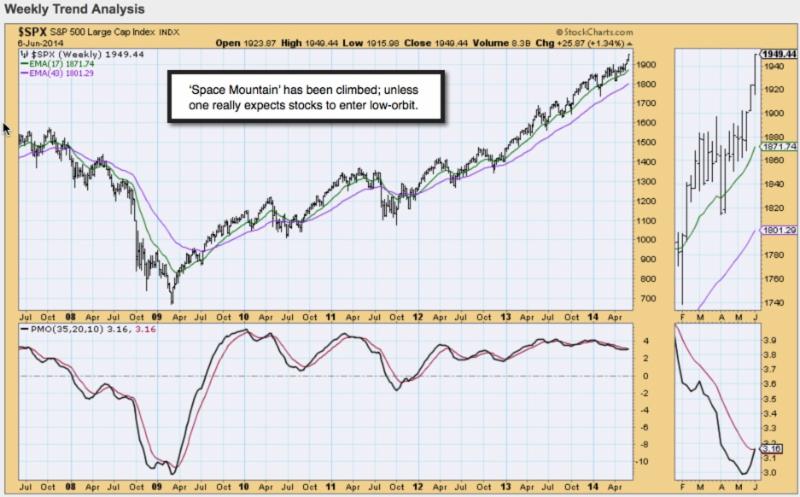

Complacency 'spun' as 'the new neutral' - is the latest explanation for why clear-sailing persists, as the market continues climbing a mountain. Even the Matterhorn has a peak; descending from it will encounter peaks and valleys for sure; but beyond a summit, one can extrapolate (factors we analyze).

There 'is' a long-term distrust of markets; while paranoia has evaporated quite a bit, if not in traders minds, in terms of 'willingness' to resist upside thrusts. That means 'excess value' will become visible more so in retrospect; as while many do not see risk in-absence of a cataclysmic event, there's something else missing:

If (what's assessed) is a 'sense' out there, isn't that capitulation? Technicians embrace 'change'; using an old saw of 'discipline' to rationalize being bullish again; in absence of real underlying basis, aside prices moving up (absent metrics; actual increases in risk arise, even though I understand not 'fighting the tape'). In essence our 'not fighting the tape' approach is shorting (fading) rallies; not at all getting excited about downside activity as underway; even intraday. That's a way to hold core investment-grade longs (as outlined), and step-aside our E-Mini S&P short-sale guidelines mostly with intraday gains.

Meanwhile, investment funds are squirreled-away pending genuine attractive valuations, as likely remain sometime-off given a degree of excess that is going to need adjustment. Market duration of 'overbought' readings is not historic; however that's the NYSE not NASDAQ or Russell. So rather than the smaller stocks simply catching-up (they're trying), we're a bit more concerned about it as a late-stage aspect in this phase (note historic chart comparison).

Daily action - elicits a throw-in-the-towel mentality that discards worry about exuberance; even expansion of the Federal Reserve's balance sheet; or the nature of the flow of liquidity that provides the impetus for the overall 'run'.

Discarding hurtles for an end-point for the Fed's unwind, and where stocks would trade, based on 'organic' values without the financially-engineered lift, should be sobering, but isn't. That will likely all be clear in-retrospect (details;

interpretations and projections of rare unfolding technical patterns explored.)

Prior highlights follow:

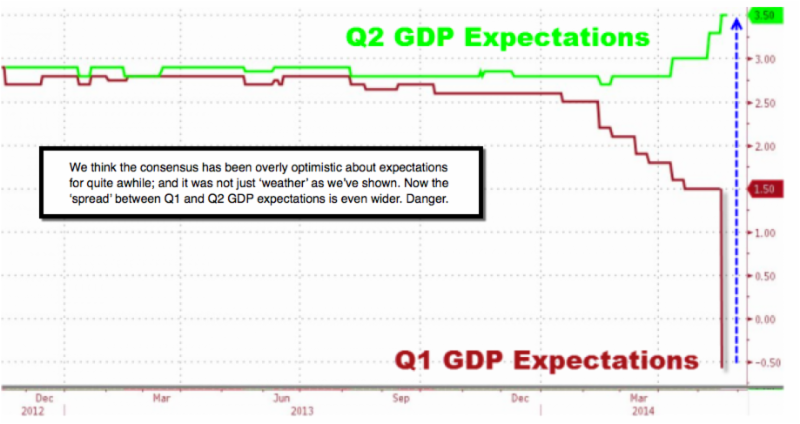

For sure it's taken longer, while both successful to trade, but frustrating for investors. And that's because of the 'low-yield-driven' backdrop we all know so well. As this compels risk-averse investors into more speculative tactics, it actually contributes to setting-up extensive purges, once (more analysis).

There are hard challenges ahead; and this time, requiring sobriety in fiscal and monetary policies; beyond financially-engineered moves.

Enjoy the weekend!

Gene

Gene Inger

www.ingerletter.com