In the previous week, the markets were expected to remain mostly volatile and to remain under range-bound oscillation without making any significant headway. In line with this analysis, the NIFTY headed nowhere, had a lackluster week and ended with mild gains on a weekly note. While the NIFTY continued to resist its important double top resistance in the zones of 11840-11880, the index finished the week with gains of 64.75 points (+0.55%) on a week-to-week basis.

We have a domestic event (the Union Budget) to face, which is slated to come on July 5th. It is important to note that, instead of the customary Vote-on-Account that a Government usually presents before the election, the Government had given a full-fledged budget. The upcoming Budget is likely to remain a continuation of what the Government has already presented, along with a few additional measures here or there.

Having said this, the Union Budget has been an overhyped event this time and is likely to remain a non-event to a greater extent. However, this event is set to cause a lot of volatility in the markets in the form of knee-jerk reactions.

We expect a quiet start to the week. The broader technical setup remains challenging and, because of the Union Budget, the range that the markets may trade in the coming week is likely to remain wider. The levels of 11950 and 12080 will be the possible resistance points. The supports will come in at 11710 and 11530.

The weekly RSI stands at 60.46; it remains neutral and does not show any divergence against the price. However, upon visual inspection, it appears to be making lower tops within a pattern formation. The weekly MACD is bullish, but it is sharply moving towards a negative crossover over the coming days. No significant structures are seen on the candles.

All in all, we may see measured up moves in the coming week. However, they are likely to remain intermittent and sporadic in nature. The broader technical setup makes it evident that quickly navigating the higher levels will not be a cakewalk for the markets, especially as the markets stay at elevated levels, with VIX trading at multi-month lows. This complacency, especially when the more extensive technical setup remaining challenging, is likely to make smooth up moves difficult.

We recommend continuing to approach markets cautiously and keeping exposures at modest levels. A highly selective approach is advised for the coming week.

Sector Analysis for the Coming Week

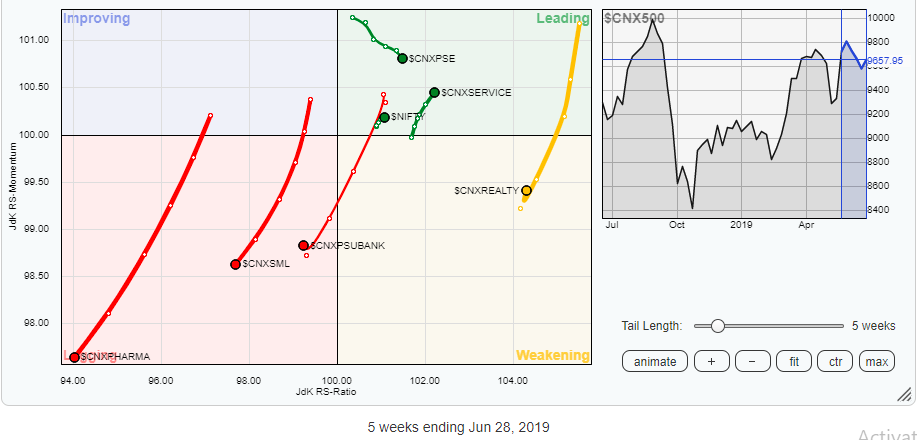

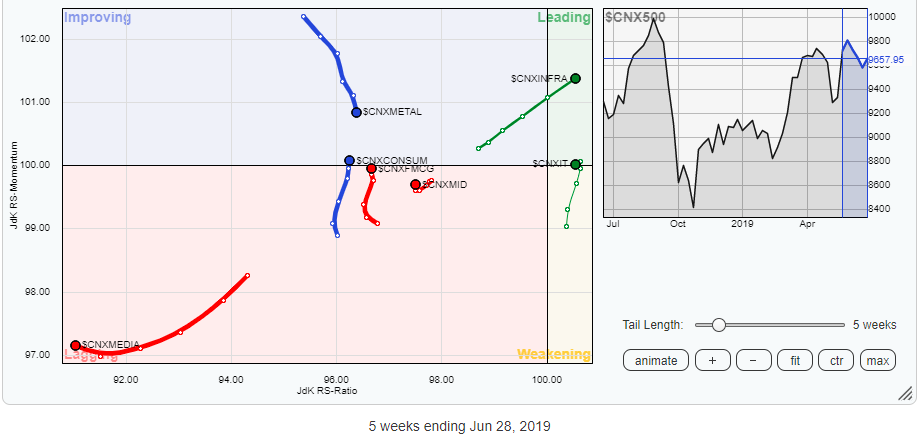

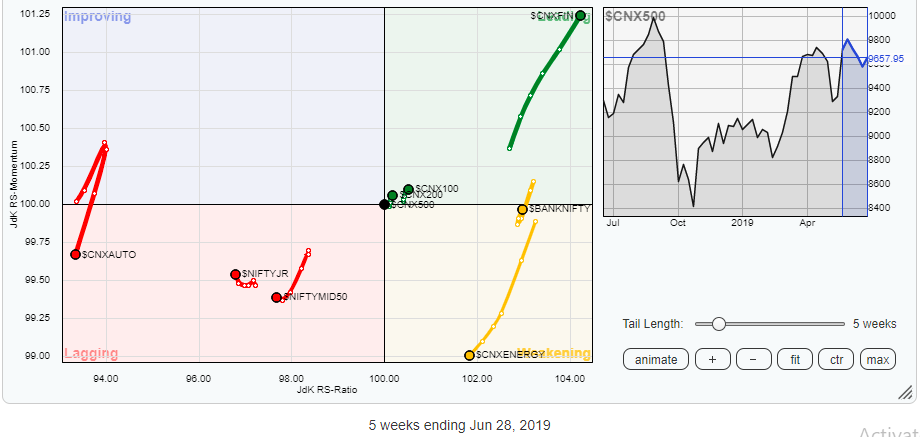

In our look at Relative Rotation Graphs, we compared various sectors against CNX500, which represents over 95% of the free float market cap of all the stocks listed.

The review of Relative Rotation Graphs (RRG) shows that the Financial Services group has continued to post consistent relative outperformance against the broader markets. It remains firmly placed in the leading quadrant. Along with this, we see the Infrastructure Index crawling further into the leading quadrant. Giving it company in that quadrant are the PSE and the Services Sector index. These groups collectively are likely to show relative outperformance against the broader markets.

The Consumption Index has crawled into the improving quadrant. Closely following it is the FMCG Index, which remains on the border while staying in the lagging quadrant. The Metal Index is seen losing its momentum and heading southward while remaining in the improving quadrant.

Meanwhile, the Auto, Energy, Media, Pharma and Realty groups are continuing to lose momentum steadily, despite minor upticks. No significant relative out-performance is expected from these packs.

Important Note: RRG™ charts show you the relative strength and momentum for a group of stocks. In the above chart, they show relative performance against NIFTY500 Index (Broader Markets) and should not be used directly as buy or sell signals.

Milan Vaishnav, CMT, MSTA

Consulting Technical Analyst

www.EquityResearch.asia