Photo by Eric Prouzet on Unsplash

Photo by Eric Prouzet on Unsplash

The Bureau of Labor Statistics released its October jobs report today. The number of jobs added was higher than the consensus forecasts.

Key Points of October Jobs Report

- Non-farm payrolls rose by 261,000 in October, higher than the 200,000 economists expected.

- Average hourly earnings were up 0.4%, which is a 4.7% year-over-year increase.

- The unemployment rate came in at 3.7%, slightly higher than the 3.5% from last month.

- Labor force participation, that is, the number of people working or looking for work, was 62.2%—a minuscule one-tenth of a point decline from September.

Overall, the numbers suggest the labor market is still hot, but may be softening ever-so-slightly. Under normal circumstances, a slowdown in job growth doesn't paint a positive picture. But because we're in a rising interest rate environment after a decade-long period of low-interest rates, the market liked what it heard.

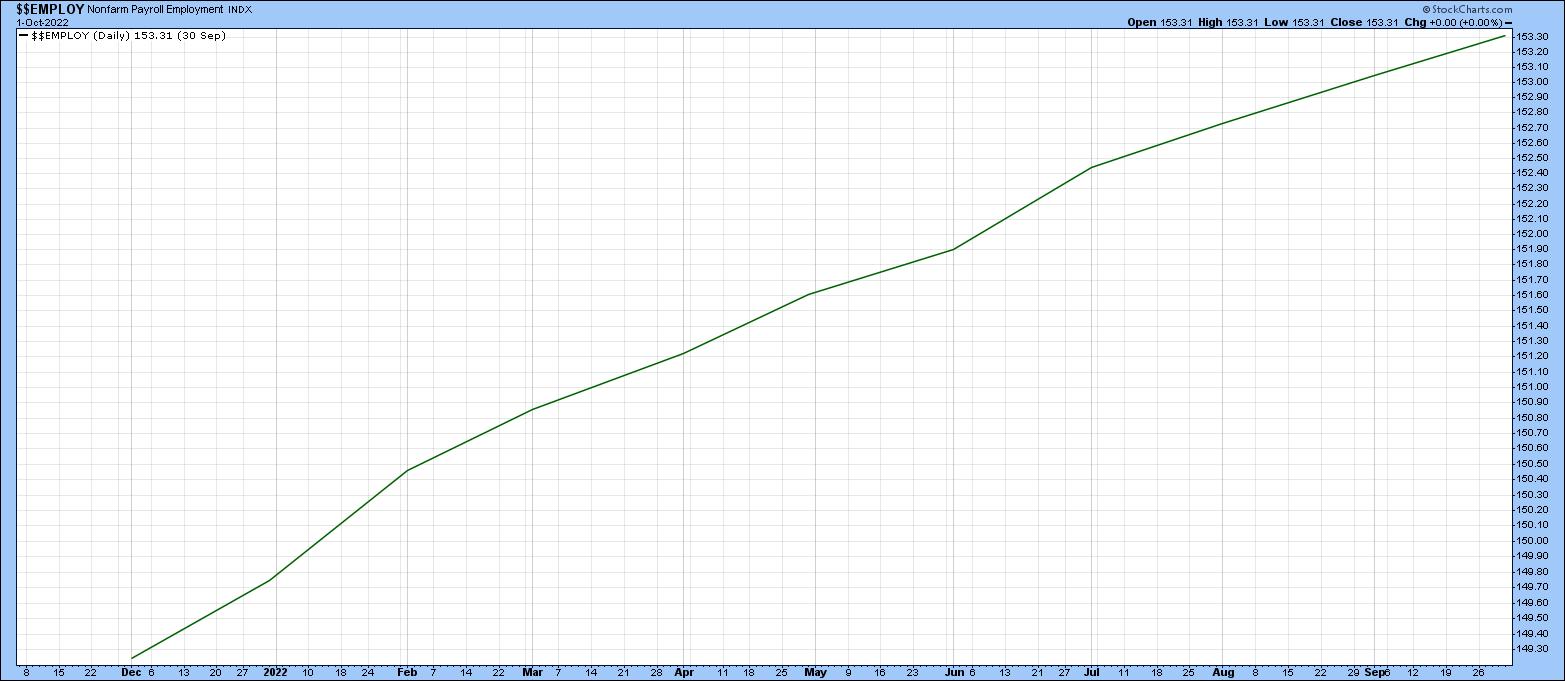

CHART 1: THE LABOR MARKET IS STILL GOING STRONG. A flattening of the non-farm payroll employment index ($$EMPLOY) could mean a softening of the labor market. Chart source: StockCharts.com. For illustrative purposes.Now, on to the Deets

On Wednesday, when Fed Chairman Jerome Powell took to the podium, he mentioned that the tight labor market is putting pressure on inflation. Although the jobs market is still tight, today's data suggests that conditions might be loosening. It's very slight, but the market acted like it'll take anything it gets.

Unemployment rose slightly, as did labor force participation. More important is the September data revision. Instead of the 263,000 jobs reported, the number was revised higher to 315,000. Relative to the revised September increase, October's increase of 261,000 jobs gave the impression, that relative to the September report, the job market is much cooler.

Could today's jobs data be an indication that the Fed may start slowing down the pace of interest rate hikes? The markets seemed to think so. Equity futures rose before the open, while the Dow Jones Industrial Average ($INDU), S&P 500 Index ($SPX), and Nasdaq Composite ($COMPQ) rose after the open, as did Bitcoin ($BTCUSD). The December 2022 U.S. Dollar Index ($USD) initially fell on the news.

Initial reactions don't necessarily paint an accurate picture of overall investor bias. The $SPX, $INDU, and $COMPQ gave up a large portion of their earlier gains, although they had recovered by Friday's close. Price action for $BTCUSD was similar to the broader equity indexes. The leading sector today was Materials, followed by Financials, and then Technology. The 10-Year U.S. Treasury Yield Index ($TNX) was relatively flat during the trading day. Overall, a good end to the trading week.

What Does This Mean for the U.S. Economy?

One month's data doesn't necessarily mean there's enough of a softening for a Fed pivot. The labor market remains tight. Employers continue to have a tough time filling positions and have to offer higher wages to attract employees.

The greatest job growth was in the healthcare industry, followed by professional and technical services. The manufacturing industry also saw robust job growth, especially in durable goods. Job growth in leisure and hospitality drew particular interest, given that the industry took a real beating during the COVID-19 pandemic. It's still not at pre-pandemic levels, but it's nice to see some growth here. Hotels added the most number of jobs in the hospitality sector. Maybe people are staying in hotels either for business or their weekend getaways.

The Fed pays close attention to the jobs report because it weighs heavily on its interest rate decisions. There probably needs to be more loosening in the job market before the Fed reduces its interest rate hike pace. A softening job market may not be great for those looking for work, but that's what needs to happen for the pace of interest rate hikes to slow down.

Next week could prove to be an exciting one for the markets. We have the midterm elections on Tuesday and the CPI report for October on Thursday. Stay tuned for our market insights and analysis on these important market-moving events.

Don't miss out on our educational content in our ChartWatchers blog, Become a seasoned StockCharts user by signing up for a one-month free trial.

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.

Happy charting!