In early December of last year, I wrote an article on whether Bitcoin had reached the tipping point in terms of signaling a peak in the crypto bubble. Some may disagree about the "bubble" label; however, it seems to me that a financial category coming out of nowhere 10-years or so ago and reaching a $3 trillion capitalization at its November 2021 peak (13% of US GDP) is an extraordinary and probably unprecedented feat. Looked at another way, the price stood at $164 in 2015 and touched $68,000 last November.

There is no doubt that the blockchain concept is sound, but so was the technology underpinning the tech bubble in the year 2,000. It was just that the prices of technology companies had got ahead of themselves. My conclusion last December was that that some cracks had begun to appear in the Bitcoin technical position, but the consensus of evidence continued to point to an uptrend. In the intervening months, the technical position has deteriorated further. Also, the charts have established some key support levels beyond which one could use to reasonably argue that the bubble has burst.

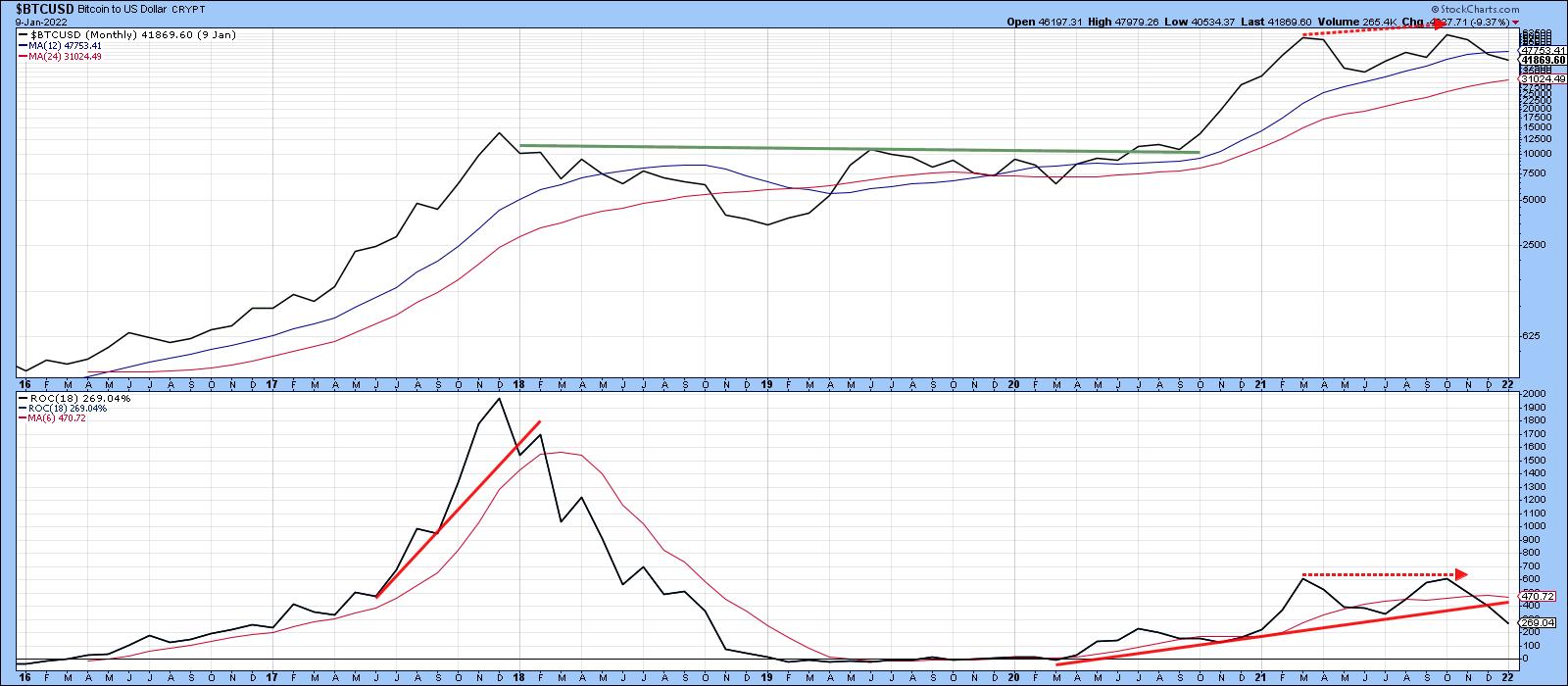

Bitcoin Momentum

One of the techniques for calling a bubble top is to observe an 18-month ROC and see when, following a lengthy advance, it reaches the 200% level and then reverses. A reading north of 200% is important because it indicates a doubling in price over a period of a year-and-a-half. Research shows that this is a very rare occurrence. For example, the very volatile copper price has only achieved it once, in the late 1970s. The S&P has never touched 200%, not even in 1929. The highest peak for any commodity, currency or stock market (not stocks), that I have ever observed was 500% for silver in 1980. My studies, covering 30+ examples spread over centuries of data, indicate that after the ROC peaks above 200%, it has taken an average of 15 years to regain the bubble high.

The reason I bring this up is that, in 2017, the ROC for Bitcoin topped out at an unprecedented 2000% and took only 3 years to recapture its losses, way shorter than the average recovery period. Chart 1 shows that the ROC has been in an uptrend since its 2020 low. The two 2021 highs clocked in at a remarkable 600%. It only looks low in the chart because of the remarkably high 2017 reading. The ROC has now set up a negative divergence with the price, because the November 2021 high surpassed that established earlier in the year. Note also that both series are below their respective MAs. More important is the fact that the ROC has recently dropped below its up trendline, thereby confirming that, as far as momentum is concerned, a reversal has taken place.

Chart 1

Chart 1

A loss of upside momentum can also be seen from Chart 2, where it is evident that the price is once again struggling in its battle to remain above its secular up trendline, as well as its 40- and 65-week MAs.

Chart 2

Chart 2

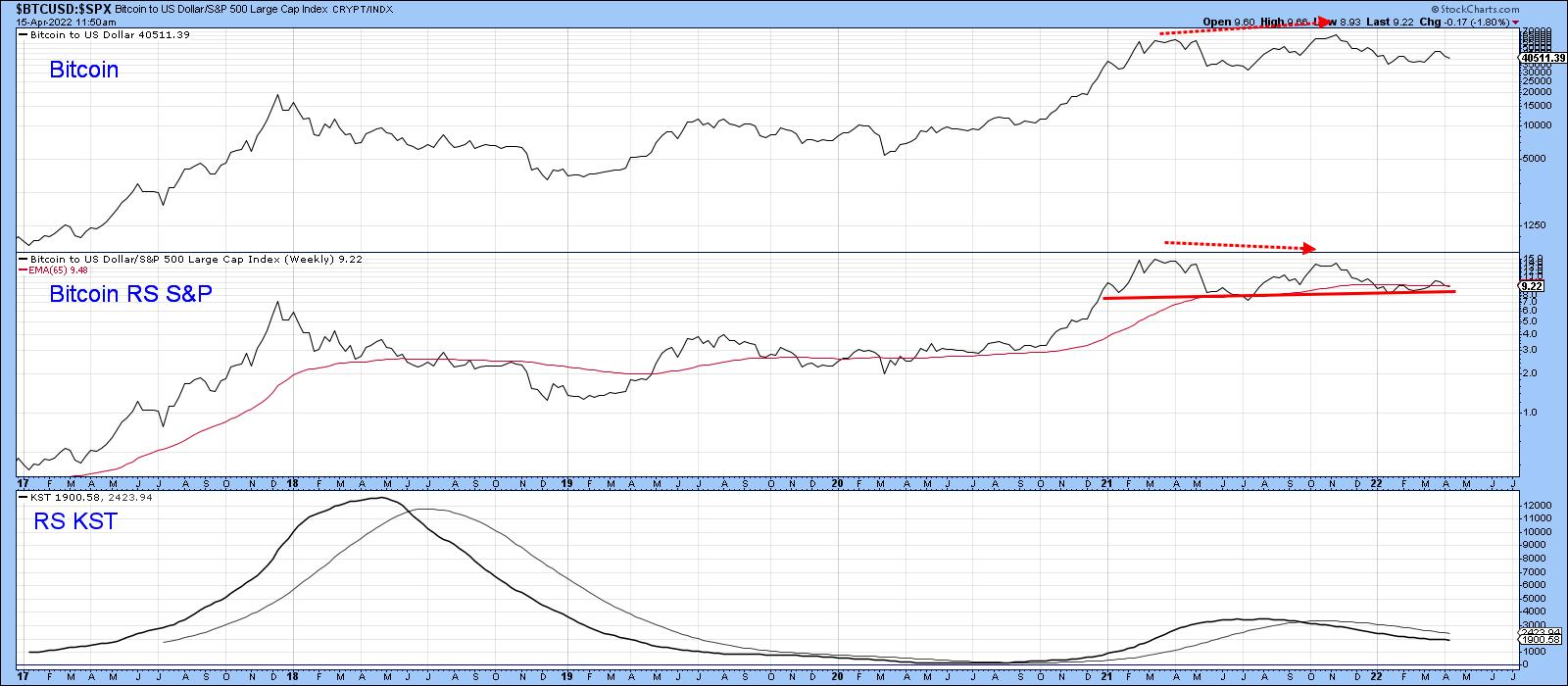

Relative Action is also Slipping

Chart 3 shows that, between 2017 and early 2021, Bitcoin was confirming every new high with a similar new high in its relative line with the S&P. The two dashed arrows indicate that was not the case in November 2021, when the price touched an unconfirmed new high, but the RS line made a lower one. It is now resting precariously on its 2021-22 support trendline. The declining KST for relative action suggests that support will soon give way.

Chart 3

Chart 3

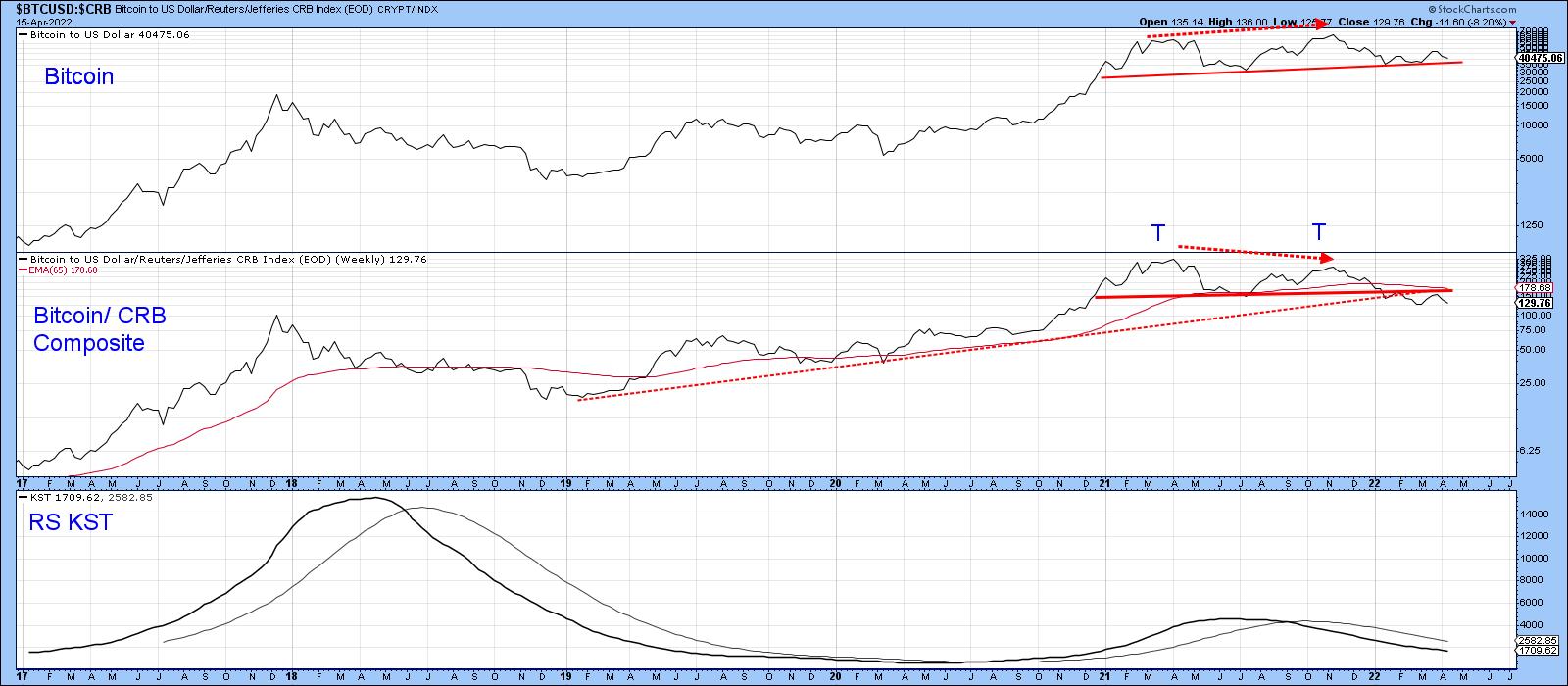

Bitcoin has also lost its mojo against commodity prices, in the form of the CRB Composite, as seen in Chart 4. In this instance, the RS line has not only diverged negatively, but has violated its (dashed) 2019-2022 up trendline and 65-week EMA. Most serious of all is the completion of a double top formation.

Chart 4

Chart 4

Price Action Looks Toppy

A basic true and tested tool in the technical arsenal is provided by peak-and-trough analysis. In that respect, Chart 5 flags the major rallies and reactions since 2019. Throughout the whole period, the series of rising peaks and troughs has been intact. That said, the most recent 2022 advance has so far failed to take out the previous peak set last November. It may well do so. All we know on that front is that the January-March rally retraced at 38% of the previous decline. That's enough to qualify the January low and March highs as legitimate benchmarks for peak-trough analysis.

Chart 5

Chart 5

Drilling down on the rally, we see a lot to be concerned about in Chart 6. One of the characteristics of a bear market advance is a false breakout from a price pattern. That's exactly what happened in late March. False breakouts are typically followed by above-average moves in the opposite direction to the breakout as traders scramble to get back on the right side of the trend, which is what appears to have been happening in the last couple of weeks. Failure of the price to clear its 200-day MA is another sign of the bear.

The level to watch now on a daily close basis is $35,000, since that marks the starting point of the 2022 rally. If that is taken out, the upward peak trough progression will be reversed, which, in all likelihood, will indicate that the November 2021 was a bubble-bursting event.

Chart 6

Chart 6

Finally, Chart 7, based on weekly data, shows the potential for a large head-and-shoulders top. Note that the recent rally failed to break above the 52-week MA. The top has not yet been completed, as that will require a Friday close under the neckline and, to be safe, a close under the January Friday close low of $35,280.

Chart 7

Chart 7

Conclusion

Bitcoin continues to experience a gradual technical deterioration, but this has not yet been confirmed with the completion of a top. When any market rises rapidly over an extended period, seemingly never to go down again, confidence naturally builds up a head of steam. That optimism results in complacency and careless decisions. With interest rates rising rapidly, potentially affecting margin accounts, now could be as good a time as any for starting to take some bets off the table.

This article is an updated version of an article previously published on Monday, April 11 at 7:09pm ET in the member-exclusive blog Martin Pring's Market Roundup.

Good luck and good charting,

Martin J. Pring

The views expressed in this article are those of the author and do not necessarily reflect the position or opinion of Pring Turner Capital Group of Walnut Creek or its affiliates.