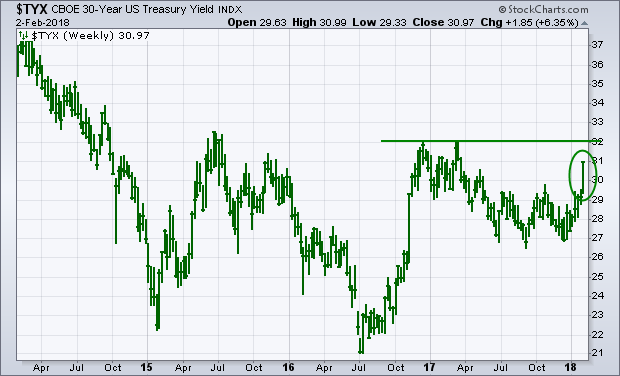

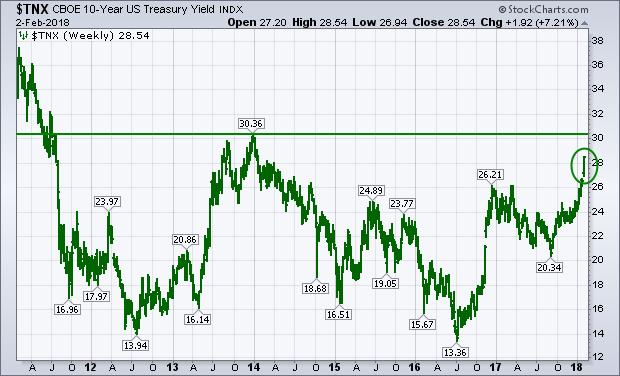

Bond yields are rising a lot faster than a lot of people expected. And that's starting to worry stock holders. The weekly bars in Chart 1 show the 30-Year Treasury Yield rising over 3.00% for the first time since last March and heading up for a challenge of its early 2017 peak near 3.20%. A close above that more important chart barrier would be very bad news for holders of long Treasury bonds which are falling. The bigger news, however, is coming from the faster rise in 10-Year yields. The weekly bars in Chart 2 show the 10-Year Treasury Yield trading at a four-year high and nearing a major challenge of its January 2014 peak near 3.03%. A decisive close above that major barrier would leave little doubt that the three decade-long bull market in bonds has ended. That's not only bad for bondholders. It may also be bad for stock holders. Current high stock valuations don't look so bad as long as bond yields stay low. They're going to look a lot more expensive if bond yields experience major upside breakouts.

The green monthly bars in Chart 3 plot a ratio of the 10-Year Treasury Yield divided by the S&P 500 over the last ten years. The falling ratio means that stocks have risen faster than bond yields throughout the nine-year bull market which has helped support rising stock prices. But not anymore. The TNX/SPX ratio bottomed in mid-2016 and has been rising since then (red box area). And it looks like it's bottoming along with bond yields. That means that for the first time since the bull market in stocks started nine years ago, bond yields are actually rising faster on a percentage basis than stocks. That's not necessarily a good sign for stocks. That's because rising bond yields make an expensive stock market look even more expensive. That doesn't mean that the uptrend in stocks is over. But it may be enough to slow down the market's advance and pave the way for higher volatility as the year goes on. We're already seeing signs of that today.

The green monthly bars in Chart 3 plot a ratio of the 10-Year Treasury Yield divided by the S&P 500 over the last ten years. The falling ratio means that stocks have risen faster than bond yields throughout the nine-year bull market which has helped support rising stock prices. But not anymore. The TNX/SPX ratio bottomed in mid-2016 and has been rising since then (red box area). And it looks like it's bottoming along with bond yields. That means that for the first time since the bull market in stocks started nine years ago, bond yields are actually rising faster on a percentage basis than stocks. That's not necessarily a good sign for stocks. That's because rising bond yields make an expensive stock market look even more expensive. That doesn't mean that the uptrend in stocks is over. But it may be enough to slow down the market's advance and pave the way for higher volatility as the year goes on. We're already seeing signs of that today.