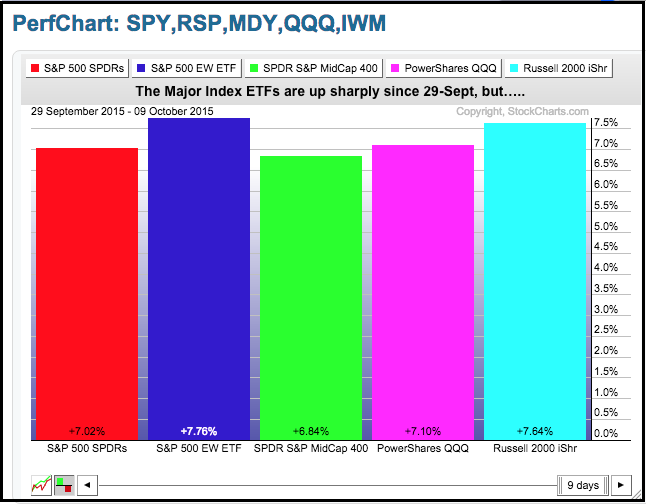

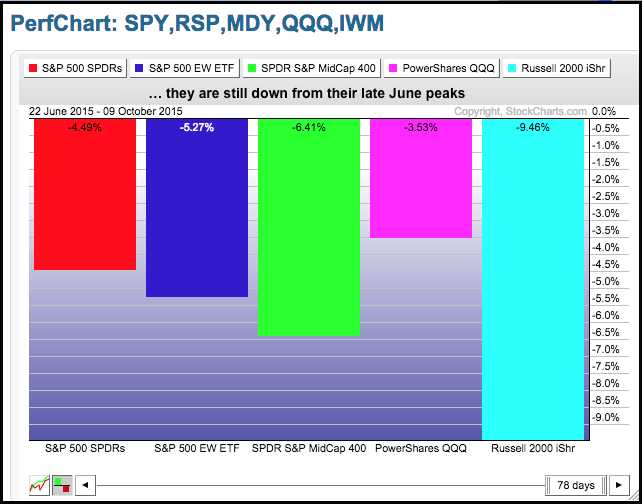

The major index ETFs are nearing their moment-of-truth as the smaller uptrends start to challenge the bigger downtrends. I am still assuming that the August breakdowns signaled the start of a bigger downtrend. While I do not know how long this downtrend will last, I have yet to get a counter signal (bullish signal). Assuming the bigger trend is down, this means smaller uptrends run counter to the bigger downtrend and the bigger downtrend is expected to take over at some point. When and where is the million-dollar question.

Raff Channels Define Short-Term Uptrends

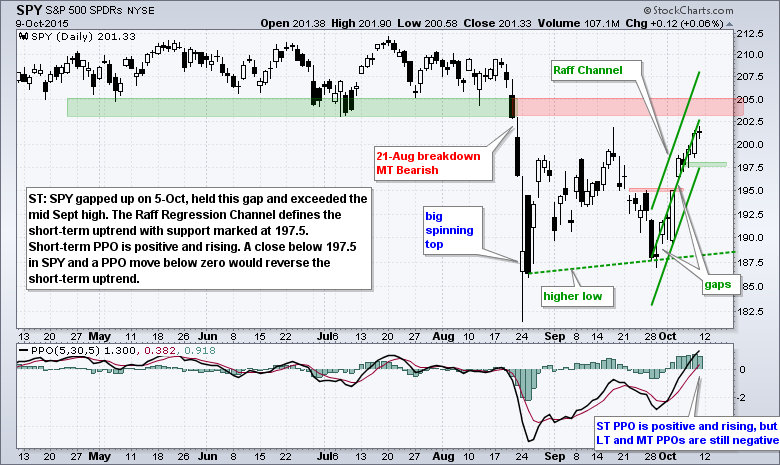

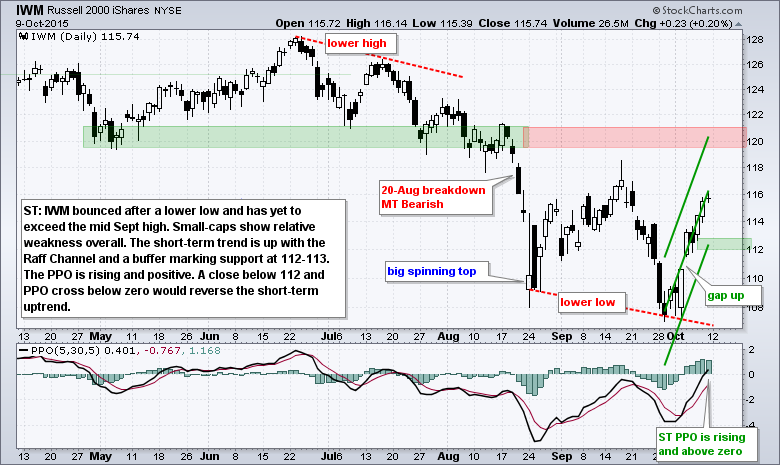

My focus is on the October surge and I am using a Raff Regression Channel to define the short-term uptrends in SPY, QQQ and IWM. The nine-day advance is rather steep and normal trend lines don't make sense. All three gapped up last Monday (5-Oct) and these gaps held all week. The PPO (5,30,5) moved up last week and turned positive for all three. Keep in mind that this is a short-term indicator. The long-term PPO (20,120,1) and medium-term PPO (10,60,1) are negative for all three and this supports my assumption for a bigger downtrend. With the bigger trend down, I favor bearish setups and signals over bullish setups and signals. A bearish setup is present right now because we have a counter-trend bounce and the short-term PPO (5,30,5) turned positive. This bearish setup would turn into a signal with support breaks and a downturn in the short-term PPO (5,30,5).

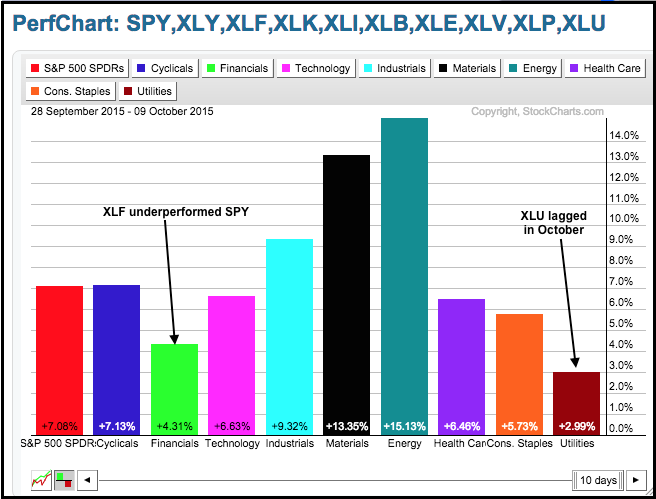

Finance and Utilities Lag in October

The three most beaten down sectors led the advance over the last two weeks. The PerfChart below shows the biggest gains coming from the Energy SPDR (XLE), Materials SPDR (XLB) and Industrials SPDR (XLI). This is a classic case of the deeper the decline and bigger the snap-back bounce. Even though the short-term moves are impressive, the bigger trends remain down for these three.

Elsewhere, notice that the Finance SPDR (XLF) and the Utilities SPDR (XLU) showed relative weakness over the last two weeks. They were up, but up much less than the broader market and the other sectors. I am especially concerned with relative weakness in the finance sector because this means large-cap banks are underperforming.

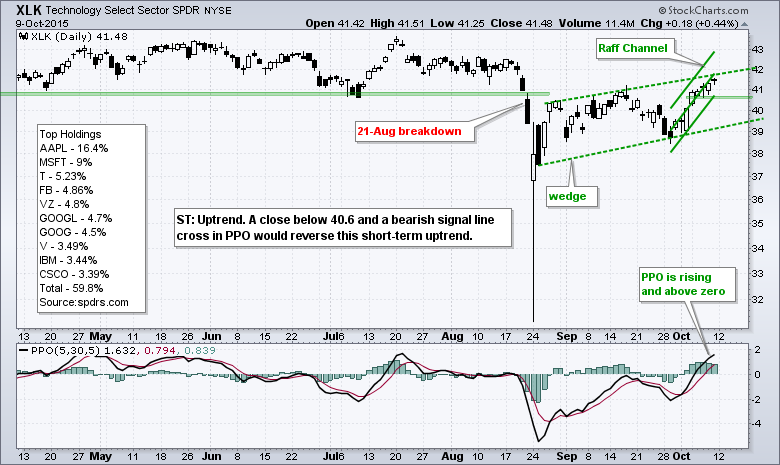

XLY and XLK Lead with Higher High

The Consumer Discretionary SPDR (XLY) and the Technology SPDR (XLK) are two of the strongest sector SPDRs overall. XLY exceeded its mid September closing high and XLK exceeded its mid September intraday high. Despite higher highs and higher lows since late August, I am watching the two week upswing for the first signs of weakness. The Raff Regression Channel and mid week lows mark first support.

Finance Falls Short

The Finance SPDR (XLF) bounced in early October, but this was one of the weakest bounces of the nine sector SPDRs. XLF did not exceed its mid September high and the percentage gain was the second weakest. The bigger trend is down and the ETF is hitting resistance in the 23.50 area.

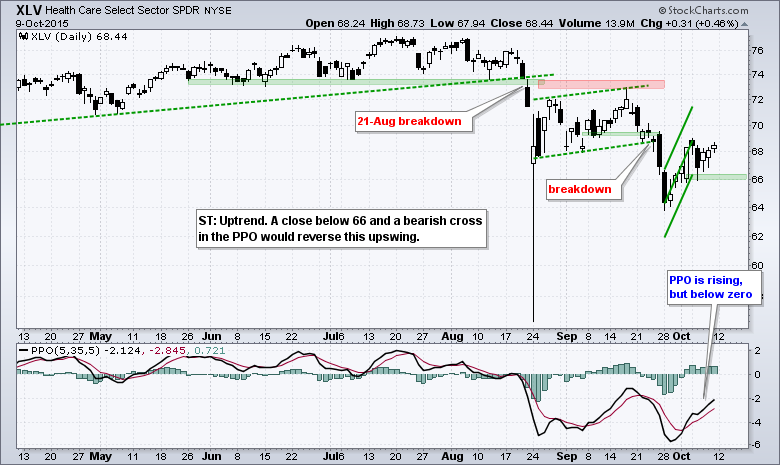

Healthcare Remains Sick

The HealthCare SPDR (XLV) bounced in October, but did not get close to its mid September high and did not even negate bearish signals on 22-Sept. This sector shows some serious relative weakness right now and the bigger trend is clearly down. The two week trend is up with support set at 66.

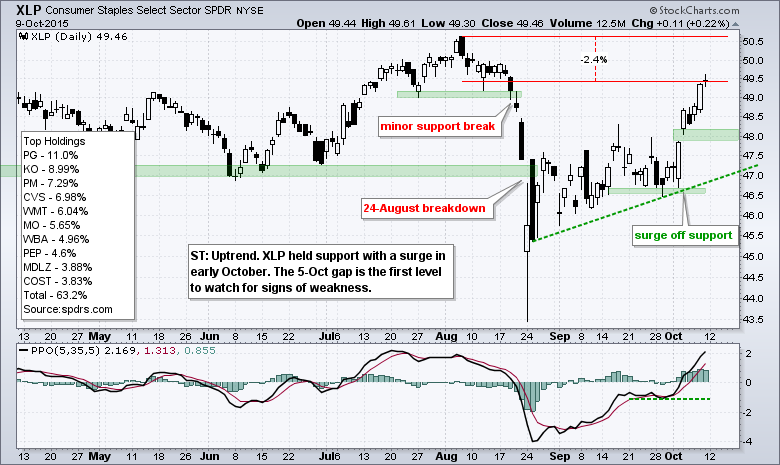

Staples and Utilities Trend Higher

The Consumer Staples SPDR (XLP) and the Utilities SPDR (XLU) held up well in September and moved to new highs for the move last week. XLP is within 3% of a 52-week high and could be considered in a long-term uptrend. In contrast, XLU is still 9% below its 2015 high and well below its August high. Even though the short-term trend is up for XLU, I still think the long-term trend is down and I am wary of this short-term uptrend.

ITB Hits Moment-of-Truth

Even though XLY exceeded its mid September high (closing basis), the Home Construction iShares (ITB) and Retail SPDR (XRT) have yet to exceed this benchmark high and continue to lag. These two industry groups are very important parts of the consumer discretionary sector. ITB is back above the 200-day moving average, but still well below its mid September high and in a downtrend overall. The short-term trend is up with the October surge and I am marking first support at 26.9.

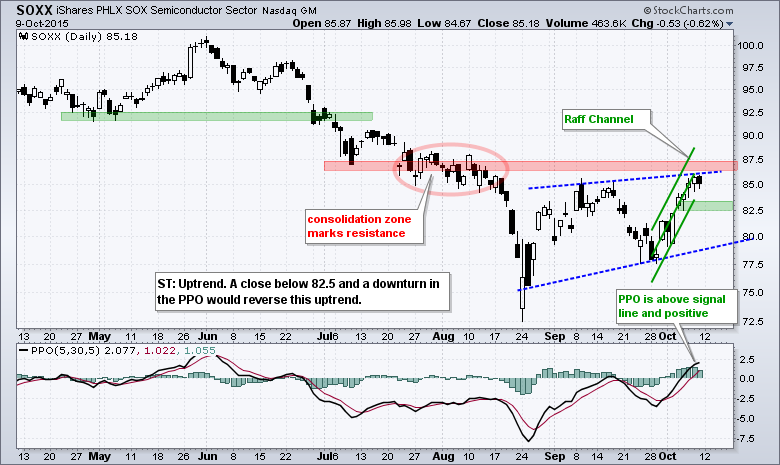

Internet and Semis Lead Tech Sector

The Internet ETF (FDN) and Semiconductor iShares (SOXX) led the tech sector with 9% advances the last nine days. Both remain in short-term uptrends and I am using the Raff Regression Channel to define this move. Channel breaks and bearish signals from the PPO would be reverse the short-term uptrends.

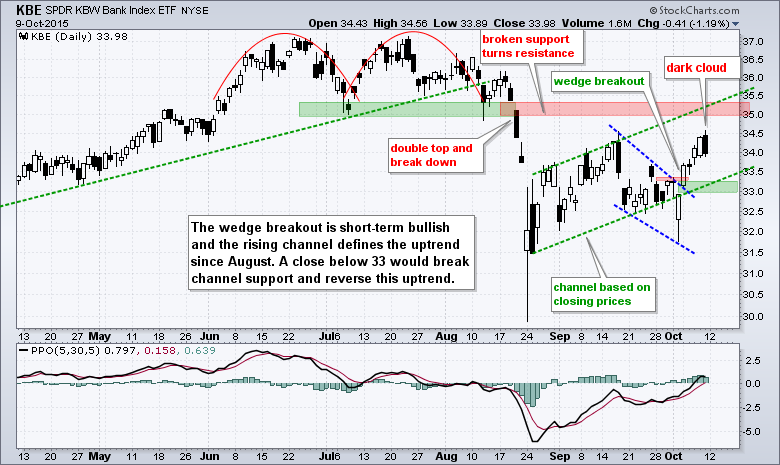

Dark Cloud and Engulfing Hit Banking ETFs

The Bank SPDR (KBE) and Regional Bank SPDR (KRE) exceeded their mid September highs last week, but ended the week on a sour note as bearish candlestick patterns formed. KBE formed a bearish engulfing and KRE formed a dark cloud. This short-term candlestick patterns have yet to be confirmed with further weakness and the wedge breakouts are still holding. I am, however, raising support and watching these two closely.

****************************************

Thanks for tuning in and have a good day!

--Arthur Hill CMT

Plan your Trade and Trade your Plan

****************************************